Two recent political crises and the present economic one illustrate the importance of the stakes involved in the paper industry. Normal capitalist conditions are not usually conducive to discussions on freedom of the press which reveal as clearly the material base of this freedom: paper, the raw material of journalism, and its control.

For the three years during the Popular Unity government in Chile one of the principal fronts in the information battle was the discussion on the nationalization of the paper industry. It should be kept in mind that the riches of Chile’s forests represent Chile’s second biggest export industry and source of foreign currency, after copper. The paper industry belonged to a monopoly owned by Jorge Alessandri, a former President of the Republic presently serving as the President of the military dictatorship’s State Council, who at all times has been closely connected to Chile’s biggest daily newspaper, El Mercurie. At that time, the conservative forces accused the government of trying to control the economic infrastructure to muzzle opposition voices. Taking into account the specific characteristics of this industry, Allende had proposed the creation of a Paper Institute where all the press and publishing groups would have been proportionally represented, and where prices would have been established. The nationalization project never saw the light of day. The paper monopoly cut back production, sabotaged distribution, and forced a substantial number of small and medium-sized printers to go bankrupt, which, of course, turned them against the Popular Unity government.

In revolutionary Portugal a similar battle was waged on the same front. During the Caetano government Eximbank and the First National City Bank had granted a loan of several million dollars for the development of the Portuguese paper industry. When the Republica newspaper affair began the two banks announced the indefinite postponement of the installation of the equipment which was already crated awaiting delivery in Helsinki. What a paradox that this very city at the same time was the site of the agreements on the free flow of ideas and information!

But political crises in themselves are not enough to see the real stakes involved. In 1973, the price of newsprint on the world capitalist market skyrocketed (more than a 75% increase in nine months, without taking into account the black market). The cost of energy, which in turn had repercussions on production and shipping costs, and inflation, were all given as reasons justifying the excessive rise in prices. These false arguments, however, hardly touched the paper industrialists, who after a period of overproduction in the sixties followed up by creating the uncertainty of future stock supply and consumer panic. The official announcement of the “paper crisis” began a period of stock-taking and vast reorganization which revealed the economic rationality of the big producers.

In Colombia, for example, North American companies, sometimes with local capitalists, control almost 80% of paper production. It has three tissue-paper factories, and can satisfy its own needs for this material. Although Colombia also has a cigarette-paper factory which supplies the countries of the Andean Group, and manufactures and exports cardboard and high-quality paper to the United States and Latin American countries, it must import all of its newsprint. In France, on the one hand, the production of newsprint fell from 430,000 tons in 1970 to around 280,000 in 1973, while on the other hand, exports of high-quality paper increased. This logic of profitability points out in sharp relief the irrationality of such choices, especially in light of national independence. France, in spite of its large forests, in 1973 imported more than 60% of its newsprint and 46% of its paper pulp. The effects of this “massive disinvestment” policy (the term used by the labor union CGT) which relied on imports, were soon felt. Foreign wood producers began to prefer to export to France the finished paper product rather than the paper pulp, as they did before.

A Very Concentrated Industry

There are few countries which produce paper. This is a characteristic common to both the paper and oil industries. One can therefore see a certain similarity in the paper crisis and oil crisis. However, the resemblance stops there. Unlike the oil industry, the countries which produce paper are all highly industrialized. Forest resources are the only raw material which, until recently, the imperialist powers overlooked in their plundering of the Third World. In 1973, 55% of the world’s forests were located in underdeveloped countries, but they produced ‘ scarcely more than 7 to 9% of the world supply of paper and paper pulp. Latin America, with almost one-fourth of the world’s forest resources, only produced 6% and Africa fluctuated between 1 and 2%. Canada and the United States alone provided around 43% of the world supply; capitalist Europe, 27%; and the rest came principally from Japan (about 10%) and the socialist countries.

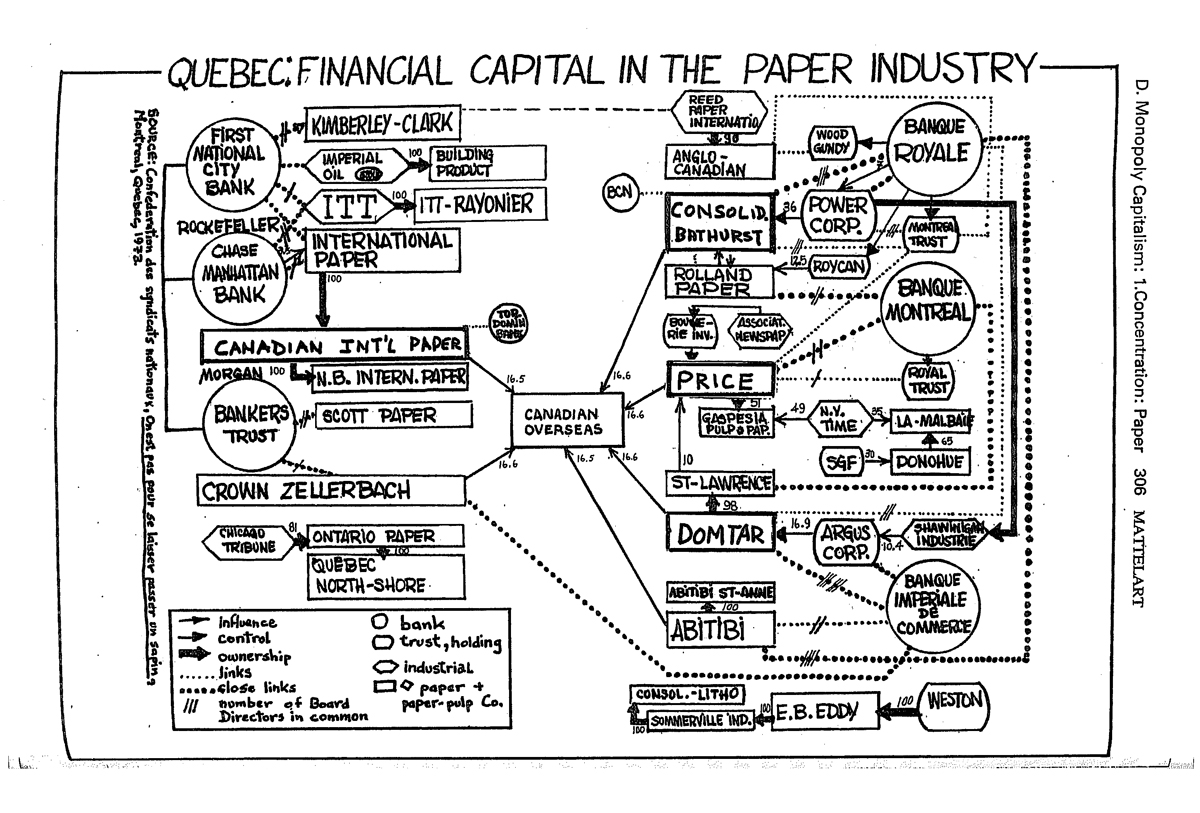

In the capitalist producing countries the paper industry is in the hands of a very small number of companies. In this respect, Quebec is a very good example. Canada is by far the world’s largest producer of newsprint: in 1970, of the 23 million tons of newsprint produced in the capitalist countries, 8.6 million was produced by Canada. Of this quantity, 44% was produced in Quebec, and it thus furnished the capitalist world with 18% of its newsprint. In this very same Quebec, more than 80% of the forest concessions were held by five big companies: two branches of U.S. multinationals (ITT and International Paper), an English group, and two Canadian firms. ITT and International Paper—two pillars of the Rockefeller empire—alone held 42.5% of the forest concessions in Quebec, a territory four times the size of Belgium.

While ITT entered the industry quite recently, International Paper began in 1910, and was the first multinational operation in the U.S. paper industry. After having used up its own forests, the United States realized that instead of importing the raw wood and manufacturing the paper at home, it would be less expensive to produce the newsprint it needed in Canada. For more than 60 years, International Paper fixed the movement of paper prices, in spite of the common front set up by its Canadian competitors. Since its beginning in 1910, this company has come a long way: in 1977 it owns 25 factories in Canada, Europe and South America.

On the capitalist world market, with the exception of two British companies firmly implanted in Canada and the United States (Bowater and Reed International, each with a turnover of around 2.5 billion dollars), the fifteen most important producers of paper have their headquarters in North America. The most important is obviously International Paper, with a turnover of more than 3 billion dollars. Two European firms are sixteenth and seventeenth in line: a Swedish firm, Svenska Cellulosa, and a French firm, Begin-Say, with a turnover of 800 million dollars.

The New Alliances

Newspaper owners were the first to look for a way of protecting themselves against the paper crisis. Horizontal integration between paper producers and big publishers has become a god of primary importance. This, in turn, has become another element accelerating the concentration of the press.

Already, dining the thirties crisis, the Hearst group, to the great displeasure of the Canadian producers, surmounted its difficulties by forming a partnership with the Quebec branch of International Paper. Since 1970, one can hardly keep track of the large North American newspapers which have established similar mergers with the paper industry. The New York Times, Washington Post, the Gannet chain (which has bought up more than 50 regional newspapers in recent years) the Newhouse group (Vogue, Mademoiselle, Glamour), Dow Jones, (Wall Street Journal), and the Chicago Tribune have all advanced to the rank of owner or major stockholder in large newsprint firms in Canada, particularly in Quebec. Others have turned towards Mexico, where they have installed factories to recycle newsprint. The Time-Life group first became interested in the future of wood in the fifties, so much so that by 1977 forest and paper operations accounted for more than half of its turnover.

These types of mergers can only be understood within the larger context of the vast reorganization of the entire media industry: newspaper concentration, computerization, and the diversification of the newspaper corporations which have taken over or created publishing houses and moved into the audiovisual market. The same type of rapprochement took place earlier in the electronics field, where the manufacturers of hardware moved into the production of software programming.

The same partnership model between the paper and newspaper industry is also found in Great Britain. In 1969, for example, Reed International took over the press group IPC (International Publishing Corporation), owners of the Daily Mirror chain distributed throughout the Commonwealth. This model has also been exported. In Brazil and Argentina, the big newspaper publishers (O Estado de Sao Paulo, for example) are closely linked to large foreign and domestic paper companies. In other capitalist countries, this kind of partnership is not as frequent, though the crisis has accelerated the rendezvous between the written press and the paper industry. Often there is a mediation between the parties which avoids the somewhat brutal aspects of monopolization found in the United States. The important national actions organized by the French labor unions during February 1977 against a government project for restructuring the paper industry indicates that this is a very timely issue.

New Producers?

One way of preventing paper shortages is the exodus towards the peripheral countries.1 Many factors contribute to this movement: the decreasing forest resources in the metropolis countries; the excessive anti-pollution laws (costing an average of around 30% of the fixed investment needed to set up a factory) in the metropolis countries;2 the shorter growing period on tropical plantations which reduces the period of maturity by 2 to 3 times (depending on conditions); and the lower wage scale and less frequent strike action (in the last four years Canadian producers have been particularly affected by lumberjack and wood worker strikes). This exodus could completely alter the map of world paper and paper-pulp production in the coming decades.

The great wave of investment is being directed toward Brazil and the southern cone of Latin America. Most of the firms which have established operations there have done so because of their approval of the geopolitical concepts of the military regimes, and thus they are directing their interest simultaneously toward Brazil, Chile and Argentina. The response to this new decentralized investment policy can be seen in the Chilean military’s recent offer of several Chilean paper firms to large North American paper companies. Needless to say, this was done without any protest from the same bourgeoisie which screamed about the violation of press freedom under Allende! In Brazil, the huge forests in the Amazon are inspiring extremely ambitious projects. If Brazil completes its program, it will be able to export 2 million tons of cellulose in 1980, and almost 20 million tons in 2000, nearly three-fourths of capitalist Europe’s cellulose production in 1973. West Africa is another region planned for development; large projects are underway in Nigeria and Gabon, for example.

Who are the promoters of these projects? Unlike the period when colonial powers could do as they pleased in plundering natural resources, today they form joint ventures in partnership with national companies to prevent possible nationalization. Once again the same old faces are there. In Nigeria, a Canadian firm, a Norwegian firm, a French firm, and International Paper. In Gabon, the French oil monopoly Elf Erap, and a Swedish firm. In French Guiana, France has asked International Paper to study the possibilities of exploiting that region’s forests. In Brazil, where the Japanese company Marubani alone has invested more than one billion dollars in a cellulose production plant, one finds all the Finnish, Swedish, Canadian and North American companies as well.

The latest protective measure against future paper risks is the change in the paper manufacturers themselves, from a traditional producer of a single item to a diversified company with many activities. In its 1975 annual report, International Paper defined its basic resource as “Land, with forests above and oil, gas and minerals below.” Putting their money where their resources are, in the same year they purchased General Crude Oil. Although horizontal integration is on the agenda as a means of facing the “global energy crisis”, obviously this only applies to the very biggest companies.

This text was originally published in Le Monde Diplomatique (Paris), May 1977. It was translated from the French by Colleen Roach. It was subsequently published in Communication and Class Struggle, Volume 1, International General, 1979.

In 1973, FAO predicted a paper and cardboard shortage of 4.9 million tons in 1977 and 9.5 million tons in 1979. ↩

In 1976, North American paper industrialists, in particular, protested against the environmental protection laws. In 1976, anti-pollution costs were 3 billion dollars, and the industrialists estimated that to comply with existing standards would cost 12 billion dollars. ↩